My Candid Take - MELI

Q1 2026

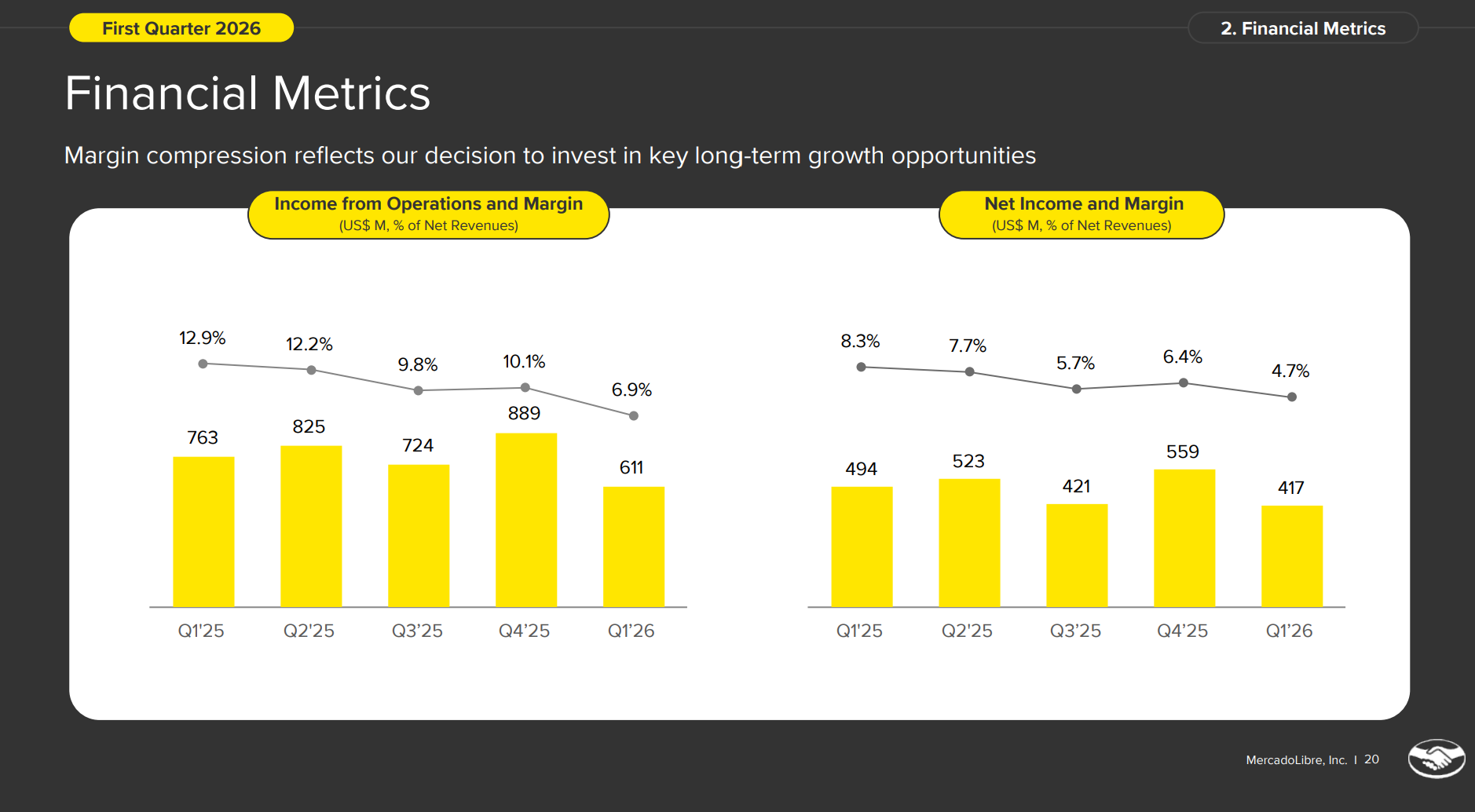

On the surface, Mercado Libre’s margin compression reads as extremely concerning. Right away, very scary questions come bubbling up– competition, bad loans, irresponsible or forced spending, etc. Margins moving straight down are typically the exact opposite of what any investor wants to see.

But if you look one layer down, you begin to see that the margin compression is not a product of external forces. Rather, it is engineered with intent. It is internally designed, and has functional levers attached to it. Being in a position of having your hand on your easily controllable margin lever is vastly different from being forced to battle forces that have their foot on your profit’s neck. One is a fight to the death, and the other is a calm and thoughtful choice. In Mercado Libre’s case, the market can’t tell the difference.

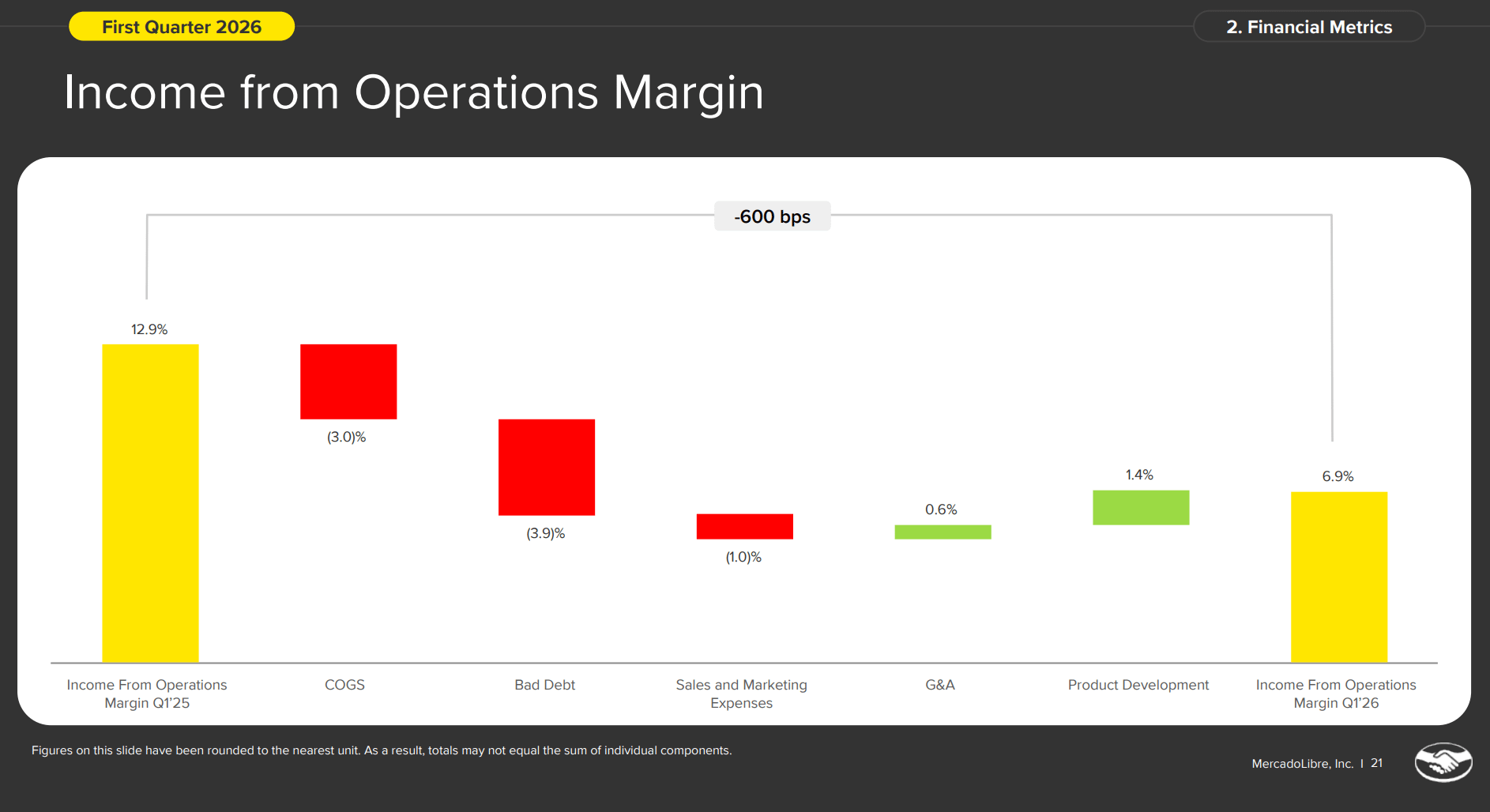

The Q1 2026 quarterly presentation shows the internal structure of the margin decline. It completely breaks it out. ‘Bad Debt’ accounts for ⅔ of the margin compression. But this is not bad debt in the traditional sense. It is (mostly) upfront provisioning for a loan book growing far more rapidly than the company’s overall revenue. And so, it is margin compression. But do you know what else it is? A choice. A tactic. A future lever on cash flows, completely controllable by the company and nobody else.

“There’s a chart on our investor presentation where we show a waterfall in terms of margin compression. There’s 4 points of margin compression because of bad debt because of the provisions. This is something that’s been happening for quite some time. The fact that our credit book grows at a faster pace than revenues, the credit book grows at 87% year-on-year and our revenues for MercadoLibre growth at 49%, that generates margin compression. And the reason for that is because as we issue any new loan, we have to provision for the full amount of the expected loss of that loan. And when we accelerate growth, we need to provision more. So 2/3 of the margin compression comes from that. That’s natural. That’s something that we have seen over time. And in fact, if you look at the credit business because it’s so profitable, it is actually accretive to margin to overall MELI. Then the 1/3 of the compression that you see on that waterfall comes from the consumer credit book in Brazil.”

– Martin de Los Santos, CFO in the earnings call

I want to be real with you— I don’t understand what kind of edge anyone needs to understand the MELI investment. Mercado Libre’s future framing is very simple in my view. A few years from now, MELI will have a GMV that is multiples of its current self. Their recently reported GMV/revenue growth rates, which aren’t just massive but are somehow accelerating, make this obvious, especially with the open-field runway sitting ahead. Attach any margin or take rate you want to that and any depressed market multiple you want to it, and you get a stock price that’s higher than today. Full stop.

Want a different framework? Operating cash flow just grew 101% YoY to $2B. The market cap is around $94B. If we dial the OCF growth way down to 5% per quarter, that means MELI is trading at a P/OCF on next year’s OCF of 10— A P/OCF of 10 for a company that just grew that same metric by over 100% in a single year. That makes no sense. It’s a disconnect of the cleanest kind.

This is the kind of fat pitch that Buffett and Munger always talked about. It’s what they call a no-brainer. As long as the investor’s mindset is truly long-term, the downside is covered, and then some.

Many investors worry about a credit event in the setting of a fickle emerging market economy. For me, this is also very simple to think about. I imagine Mercado Libre’s profits completely wiped for a year or two, or even longer. The market would be beside themselves and there would be no limit to the selling and shorting. The stock would be eviscerated.

And then there would be me, watching all this happen with my immensely crippled position, just buying and buying and buying. Why? How could I do that when every bear would have seemingly been proven right? It’s because MELI is like the salt in Latin America’s ocean. It is deeply engrained. It is an unremovable, unreplaceable part of that world. It is the economy, the culture, and the infrastructure that makes the wheels turn there— not just for the company, but for the people and families of the region. And its embeddedness is only deepening. That’s what a truly valuable asset looks like.

Then there’s the management to consider. These aren’t just good managers. These are the top of the top of the top. They are some of the smartest, savviest, most skillful operators in the entire world. So yes, I would be buying the entire time that these world-class operators, managing this immovable, deeply engrained Latin American ecosystem, worked to remodel their lending or pull levers to correct course. I would be along for the ride with zero– and I do mean zero– long-term concerns for the value of my investment. If I could buy the whole company and uninstall Yahoo Finance, I would.

Is this way of thinking about it an edge for me, or a downfall?

In a world where Walmart exists alongside Target, AWS exists alongside Azure and Google Cloud, and Costco exists alongside BJ’s, Sea Limited and other competitors will exist alongside Mercado Libre. But none of them will have the same embeddedness. None of them will so completely make up the fabric of the regions they operate in. And so I will own MELI.

Not financial advice.

If Mercado Libre stops pulling it's levers, profitability will rise but growth will also slow down, which is ok, but should also be considered. Some reinvestment will always be needed to fend off competition.

I agree that re-investment should be factored in, but saying it is priced at 10x OCF is not an accurate representation of its valuation. Meli is a mixed business, there are many pitfalls in using cash flows to value banks.

I think making adjustments to net income might be a better approach, coming up with an Owners Earnings metric.

I agree that companies (and investors) with a long-term mindset tend to outperform. Meli is a great business, the only question is valuation. It is hard to to use cash flow for Meli given the fintech side of the business will skew the numbers.

On an income-basis, what do you think is a fair value multiple for Meli?

It has great growth rates, but it is much more expensive than other companies like PDD Holdings or Kaspi.